European Economy: Hit, Not Sunk

- Due to its chronic energy deficit, Europe is particularly vulnerable to oil shock.

- However, the conditions for a broad-based surge in non-energy prices are not in place.

- Signs of a slowdown in activity are intensifying as uncertainty drags on.

- Fiscal policy no longer has the same room for maneuver as during the 2022 shock.

- By contrast, the ECB is not compelled to tighten monetary policy aggressively.

In the human body, when an artery becomes blocked, cells are deprived of oxygen and, if the problem persists, paralysis or death can ensue. The Strait of Hormuz is to the global economy what a vital artery is to the body. Around one-fifth of global oil and liquefied gas flows, as well as refined products used as inputs for industry and agriculture, pass through it.

Following the war launched by Donald Trump against Iran on February 28, this passage has been almost entirely closed for nearly three months. Visibility on the continuation of military operations or potential diplomatic initiatives remains extremely limited. Whatever the eventual outcome, a return to normal conditions will take time. These events are therefore disrupting global economic activity, particularly for countries that import oil and gas.

From this perspective, Europe is vulnerable. Its energy trade balance has been in chronic deficit for years. Approximately 6% of its crude oil imports transited through Hormuz, and just under 10% of its gas imports. With few short-term substitutes available, a surge in prices immediately inflates the energy bill. Based on current prices, the euro area’s energy trade deficit is estimated at 2.3% of GDP, up from 1.6% in 2025. This is a significant increase, though still far less dramatic than in the aftermath of the collapse in Russian gas supplies in 2022. At that time, the energy bill had doubled and exceeded 4% of GDP. A key difference between the two episodes is that the current tension is concentrated on oil prices and has had limited spillovers in gas and electricity prices.

Still, for consumers, oil prices have an immediate impact at the pump and, as a result, undermine confidence. Added to this is media commentary, which by nature gravitates toward the sensational and constantly revives memories of past shocks, whether the distant ones of the 1970s or more recent episodes, often overlooking the fundamental differences with the current situation.

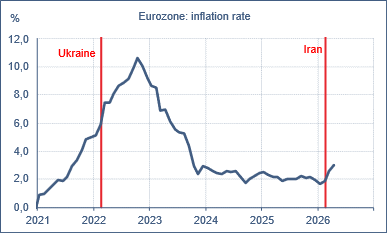

In 2022, annual inflation surged from 5% to over 10% in just a few months. More troubling still, price pressures spread across nearly all categories. This time, the starting point was much lower, with inflation below 2% before the launch of Operation “Epic Fury” (see chart). Three months later, inflation in the euro area rose to 3%. According to business surveys, competitive pressures are limiting the pass-through of the shock to final consumers. In short, economic policymakers must remain vigilant, but there is no cause for alarmism.

Source: ODDO BHF

On the fiscal front, governments face the challenge of calming public opinion while containing the cost of support measures. It is no longer possible to respond indiscriminately, as was the case during the 2022 energy crisis. At that time, the economy was emerging from the Covid crisis, when urgency had led to a general loss of fiscal discipline. It was also a world in which interest rates were so low that public debt appeared almost costless. At the European level, transfers and subsidies to households and businesses amounted to 1.9% of GDP in 2022 and 1.8% in 2023. In 2026, some support measures have been introduced, but they are targeted and modest, with a cost estimated by the ECB at just 0.1% of GDP.

On the monetary side, the current shock presents central bankers with a classic dilemma: inflationary pressures on the one hand, weaker activity on the other. Navigating between these opposing forces is no easy task. Here again, comparison with 2022 is instructive. At that time, the ECB’s policy stance was excessively accommodative, with policy rates still negative, making a tightening of monetary conditions unavoidable. Today, monetary policy is broadly balanced, calling for a more nuanced response. The ECB Governing Council has deemed it prudent to remain on hold, but several voices—particularly in Germany—are calling for a rapid rate hike. This stance appears somewhat dogmatic, as if any overshoot of the inflation targets automatically warranted an immediate response. In our view, this overestimates the risk of price spillovers and underestimates the risks of recovery.

Prior to the Gulf war, European growth was expected to reach 1.2% in 2026, following 1% in 2025. A key assumption was that the investment program launched by Chancellor Merz would inject new momentum into the German economy, which has been stagnant for several years, and generate positive spillovers for neighboring countries. In addition, with inflation normalized and unemployment low, consumers were expected to reduce their savings rate. Finally, the credit cycle, particularly in real estate, was projected to strengthen.

Since the outbreak of the war, growth forecasts have been revised downward to varying degrees depending on energy price scenarios. In a benign scenario, one from which we are already drifting somewhat, the ECB and the IMF have lowered their 2026 growth forecast by 0.3 percentage points, to 0.9%. Germany’s recovery has yet to materialize. France and Italy are facing higher debt servicing costs and have little fiscal leeway. In an adverse scenario, where the oil crisis persists for several more months, heightened pressure on confidence and spending could shave another 0.3 percentage points off growth, bringing it down to 0.6%. In a severe scenario, fortunately the least likely, where the shock becomes permanent, there would be a genuine risk of recession accompanied by a sustained rise in inflation.

In recent years, the European economy has weathered a series of negative shocks: the war in Ukraine, the inflation surge, global monetary tightening, political turbulence, and higher U.S. tariffs. The oil shock adds to this list and once again tests Europe’s capacity for adaptation. At the very least, it weakens the ongoing recovery. Leading indicators of business sentiment point in this direction, without suggesting an abrupt collapse.

Past performance is not a reliable indicator of future returns and is subject to fluctuation over time. Performance may rise or fall for investments with foreign currency exposure due to exchange rate fluctuations. Emerging markets may be subject to more political, economic or structural challenges than developed markets, which may result in a higher risk

Disclaimer

This document has been prepared by ODDO BHF for information purposes only. It does not create any obligations on the part of ODDO BHF. The opinions expressed in this document correspond to the market expectations of ODDO BHF at the time of publication. They may change according to market conditions and ODDO BHF cannot be held contractually responsible for them. Any references to single stocks have been included for illustrative purposes only. Before investing in any asset class, it is strongly recommended that potential investors make detailed enquiries about the risks to which these asset classes are exposed, in particular the risk of capital loss.

ODDO BHF

12, boulevard de la Madeleine – 75440 Paris Cedex 09 France – Phone: 33(0)1 44 51 85 00 – Fax: 33(0)1 44 51 85 10 –

www.oddo-bhf.com ODDO BHF SCA, a limited partnership limited by shares with a capital of €73,193,472 – RCS 652 027 384 Paris – approved as a credit institution by the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and registered with ORIAS as an insurance broker under number 08046444. – www.oddo-bhf.com

Author