From oil shocks to energy sovereignty: Europe confronting a new era of geopolitical tensions

This paper draws on research and analysis conducted by ODDO BHF Research.

Introduction

The conflict that erupted in the Middle East in early 2026 has triggered a significant energy shock, comparable in several respects to the major oil crises of the 1970s. The prolonged closure of the Strait of Hormuz—a strategic chokepoint for global hydrocarbon trade—has severely disrupted oil, refined products, and natural gas markets, leading to heightened price volatility and mounting supply pressures.

For Europe, these developments have once again exposed persistent structural vulnerabilities. Despite meaningful progress in recent years toward energy diversification and the energy transition, the continent remains, at this stage, highly exposed to geopolitical risk, largely due to its continued reliance on imports and limited industrial capacity in several critical segments.

Beyond short-term market imbalances, the current crisis can be viewed as a strategic wake-up call. It reinforces the relevance of Europe’s energy sovereignty agenda and raises fundamental questions about the continent’s ability to secure long-term energy supplies while remaining on track with its energy transition objectives.

A global oil shock of historic proportions

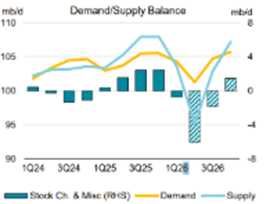

The closure of the Strait of Hormuz for more than thirteen weeks has emerged as one of the primary destabilizing forces in the global oil market. This strategic passage accounts for nearly 20% of global oil and LNG flows, making it a critical node in the international energy system. Its paralysis has resulted in a substantial supply shock, with an estimated loss of approximately 14 million barrels per day in the Middle East and more than one billion barrels of cumulative production have been foregone since the onset of the crisis. ¹

As a result, the oil market has entered a pronounced deficit phase, currently estimated at close to 6 million barrels per day.² The sharp rise in prices has already triggered an initial wave of demand destruction, estimated at around 1.3 million barrels per day.³ Initially comfortable inventory levels helped cushion the shock, as OECD countries released roughly 400 million barrels from strategic reserves.⁴ However, the progressive depletion of these stocks is now reducing this stabilizing buffer.

While markets are currently pricing in a gradual normalization—based on a central scenario involving a diplomatic resolution and the eventual resumption of flows, this outlook remains highly uncertain. Should geopolitical tensions persist, current imbalances could prove more durable, keeping oil prices structurally elevated.

Refined products: Europe’s Ddpendency comes into focus

Beyond crude oil, the crisis has also highlighted vulnerabilities in the refined products market, which has been severely impacted by disruptions to Middle Eastern refining capacity. Prior to the conflict, the region exported approximately 3.3 million barrels per day of refined products. ⁵ Targeted attacks on several refineries have led to a sharp contraction in supply, particularly in the jet fuel segment.

Exports of jet fuel to international markets have reportedly fallen sharply, driving prices to levels approaching USD 200 per barrel. ⁷ Diesel markets have also come under pressure, with prices nearing USD 175 per barrel. ⁸ These developments underscore the sensitivity of refined product markets to localized shocks and their ability to generate global ripple effects.

Europe appears particularly exposed to this environment. Nearly 60% of OECD Europe’s jet fuel imports from outside the region originate in the Middle East, ⁷ highlighting the scale of Europe’s structural refining deficit. Since 2012, the closure of 24 refineries has materially reduced domestic capacity, increasing reliance on imports. While diesel supply is somewhat more diversified, the crisis nevertheless underscores the strategic value of strengthening European refining capabilities—particularly through the development of bio-refining capacity focused on sustainable fuels such as SAF and renewable diesel.

Natural gas: relative resilience under strain

European and global natural gas markets have also been affected by the conflict that began in Iran, notably following attacks on critical gas infrastructure, including Ras Laffan. These events triggered a rapid price spike, with European TTF prices peaking around €70/MWh and Asian JKM prices reaching approximately USD 25/MMBtu. ⁹ This volatility once again illustrates the structural sensitivity of gas markets to the security of key infrastructure assets.

Unlike oil, gas exports rely on a more concentrated and less flexible infrastructure network. Qatar, a central player in the global LNG market, accounts for roughly 20% of global LNG flows and nearly 5% of global gas production. The crisis has intensified competition between Europe and Asia, with LNG cargoes increasingly diverted to the highest-priced markets.

Although some price correction has occurred, the market remains structurally tight. Europe, while better diversified than in the past due to the expansion of LNG imports, remains vulnerable—particularly as the summer period approaches. The need to replenish gas storage ahead of winter coincides with rising Asian demand, against a backdrop of the permanent loss of Russian gas imports.

A conflict that reinforces Europe’s energy sovereignty ambitions

The tensions observed across global energy markets have brought Europe’s energy sovereignty agenda back to the forefront of strategic debate. The current crisis has exposed deep-rooted dependencies, particularly in oil, refined products, and natural gas.

In oil and refined products, electrification of energy end use, especially in road transport, remains a key lever for reducing dependence on hydrocarbons. For harder-to-electrify sectors such as aviation, heavy transport, and certain industrial applications, the challenge is primarily industrial. Expanding European bio-refining capacity could, over time, enable the local production of renewable fuels, including renewable diesel and sustainable aviation fuels.

These priorities are embedded in the European regulatory framework, notably the RED III directive, which targets approximately 45% renewable energy by 2030, ¹⁰ and the ReFuelEU Aviation regulation, which mandates the progressive incorporation of sustainable fuels in aviation. However, deployment remains constrained by high costs, long industrial lead times, and significant infrastructure requirements.

In natural gas, Europe’s room for maneuver appears more limited. Domestic production, including in the North Sea, is insufficient to sustainably offset import dependence. In this context, the continued expansion of renewable energy stands out as one of the most credible long-term pathways to reducing exposure to geopolitical shocks and strengthening Europe’s energy security.

Would you like to learn more about the research analysis conducted by ODDO BHF Securities?

Sources

- https://www.iea.org/reports/oil-market-report-may-2026 “cumulative supply losses from Gulf producers already exceed 1 billion barrels with more than 14 mb/d of oil now shut in”

- https://www.iea.org/reports/oil-market-report-may-2026 (see chart below)

- https://www.iea.org/reports/oil-market-report-may-2026 “World oil demand is forecast to contract by […] 1.3 mb/d less than our pre-war forecast”

- https://www.iea.org/news/iea-member-countries-to-carry-out-largest-ever-oil-stock-release-amid-market-disruptions-from-middle-east-conflict “The 32 Member countries of the International Energy Agency unanimously agreed today to make 400 million barrels of oil from their emergency reserves available” 11 Mars 2026

- https://www.iea.org/reports/oil-market-report-march-2026 “Gulf producers exported 3.3 mb/d of refined products”

- https://economictimes.indiatimes.com/news/international/world-news/europes-jet-fuel-imports-from-middle-east-stop-raising-supply-crunch-fears/articleshow/130580010.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst “nearly 60% of OECD Europe’s jet fuel imports from outside regions came from the Middle East, according to Kpler data”

- https://thecorner.eu/interviews/in-the-last-ten-years-while-consumption-has-risen-by-1-3-24-refineries-have-been-closed-in-the-eu/102780/

- https://www.iea.org/topics/the-middle-east-and-global-energy-markets “the European benchmark for natural gas prices, rose by more than 40% between late February and late May.”

https://www.acer.europa.eu/sites/default/files/documents/Publications/ACER-LNG-Monitoring-Report-2026.pdf “recent events in the Middle East, however, have fuelled volatility and temporarily pushed TTF intraday prices above 70 EUR/MWh.” - https://energy.ec.europa.eu/topics/renewable-energy/renewable-energy-directive-targets-and-rules/renewable-energy-targets_en

Past performance is not a reliable indicator of future returns and is subject to fluctuation over time. Performance may rise or fall for investments with foreign currency exposure due to exchange rate fluctuations. Emerging markets may be subject to more political, economic or structural challenges than developed markets, which may result in a higher risk

Disclaimer

This document has been prepared by ODDO BHF for information purposes only. It does not create any obligations on the part of ODDO BHF. The opinions expressed in this document correspond to the market expectations of ODDO BHF at the time of publication. They may change according to market conditions and ODDO BHF cannot be held contractually responsible for them.

Any references to single stocks have been included for illustrative purposes only. Before investing in any asset class, it is strongly recommended that potential investors make detailed enquiries about the risks to which these asset classes are exposed, in particular the risk of capital loss.

This document is based on research produced by ODDO BHF. The analysts who contributed to its preparation are subject to ODDO BHF’s internal policies governing the production and dissemination of investment research. ODDO BHF, its entities, officers, or employees may hold positions in the financial instruments mentioned or maintain commercial relationships with the issuers concerned. A detailed and up-to-date list of potential conflicts of interest is available at the following address: Disclaimer | ODDO BHF Securities (section “conflicts of interest risk”).

ODDO BHF

12, boulevard de la Madeleine – 75440 Paris Cedex 09 France – Phone: 33(0)1 44 51 85 00 – Fax: 33(0)1 44 51 85 10 – www.oddo-bhf.com ODDO BHF SCA, a limited partnership limited by shares with a capital of €73,193,472 – RCS 652 027 384 Paris – approved as a credit institution by the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and registered with ORIAS as an insurance broker under number 08046444. – www.oddo-bhf.com

Author