Hormuz Off / Hormuz On, and the Economic Outlook

Key Messages

- While fragile, the U.S.–Iran peace framework is a constructive development.

- It reduces geopolitical uncertainty and should help ease pressure on interest rates.

- Inflation is passing its mid-2026 peak and is expected to moderate in the coming months.

- At this stage, the impact on global growth remains contained, though more pronounced in the euro area.

- The ECB’s rate hikes raise concerns about a potential policy mistake.

A geopolitical shock with lasting effects on the global economy

At times, the global economy behaves like a complex physical system: an external shock alters its conditions, yet the removal of that shock does not necessarily restore the system to its prior state. The effects can persist.

Last year provides a useful precedent. The tariffs announced by Donald Trump in early April were rapidly scaled back given their potentially destabilizing consequences. Nevertheless, the deterioration in business sentiment lingered for several months. This year, the sudden closure of the Strait of Hormuz placed the global economy under significant strain. Although a path toward de-escalation has emerged in recent days, a swift return to pre-conflict conditions—specifically those prevailing before the February 27 U.S. and Israeli strikes on Iran—should not be expected.

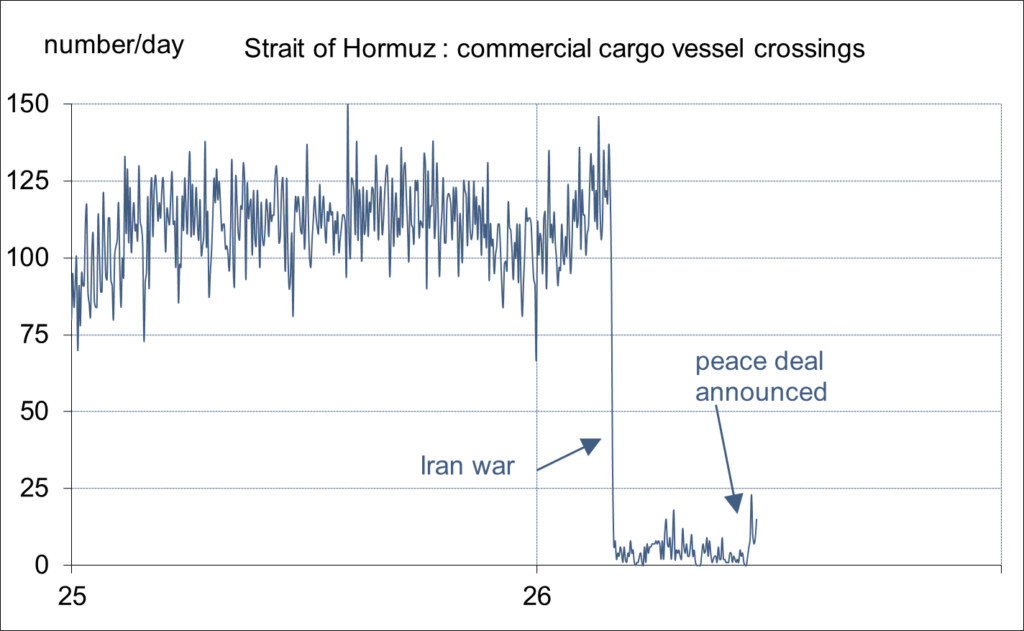

Satellite data compiled by Bloomberg indicate that approximately 110 commercial vessels transited the Strait of Hormuz daily on average in 2025. Beginning February 28, traffic dropped to near zero. Since the June 14 announcement of a memorandum of understanding between the United States and Iran, activity has gradually resumed, but volumes remain subdued (see graph). A full normalization will depend on credible security assurances for crews, including mine clearance operations, and strict adherence to ceasefire terms. This process will take time and is likely to be uneven.

Source : ODDO BHF

Oil shock better absorbed than expected thanks to market adjustments

With these caveats in mind, there is now sufficient visibility to assess the initial economic and inflationary implications, as well as the policy response.

Notably, the most dire early projections have not materialized. The International Energy Agency initially warned of the most severe oil market disruption on record, with some forecasts pointing to oil prices reaching $200 per barrel or higher, accompanied by a broad surge in commodity prices. In reality, Brent crude peaked below $120 and stands below $80 as of June 22—down one-third from its high and approximately 15% above pre-conflict levels.

Several factors explain this resilience and underscore the adaptability of the global economy. Oil flows have been partially rerouted through pipelines; strategic reserves have been deployed swiftly and at scale; and, importantly, demand has adjusted—particularly in China. Some analysts now characterize China as the marginal importer of oil, effectively acting as a “swing importer” that has helped absorb part of the shock. Prior to the conflict, the oil market was in surplus. The recent deficit appears temporary rather than structural, suggesting that the geopolitical risk premium could continue to recede.

Turning to growth, the outlook at the start of 2026 was broadly favorable. Global GDP was expected to expand at slightly above 3% in real terms, broadly in line with recent trends. The U.S. economy was operating above potential—estimated at around 2%—driven by robust capital expenditures linked to artificial intelligence. The euro area was roughly at potential (around 1%), with expectations of a recovery in Germany.

By mid-2026, real GDP growth forecasts have been revised downward by approximately 0.3–0.4 percentage points across advanced economies. Conditions are particularly concerning in the euro area, where momentum was already weak at the start of the year, even before the Middle East tensions. Recent central bank projections place growth at just 0.5% in both France and Germany—levels approaching stagnation.

Inflation dynamics had been diverging across regions prior to the conflict. In the United States, inflation had exceeded the 2% target for five consecutive years, with normalization not expected before 2027. In the euro area, inflation had already converged back to target by late 2025. The recent energy shock temporarily pushed inflation higher—from 2.4% to 4.2% in the United States between February and May, and from 1.9% to 3.2% in the euro area. This effect is now set to reverse. Declining energy prices should support disinflation in the second half of 2026, even before any second-round effects—which remain absent to date—materialize. Importantly, the magnitude and duration of this inflation spike are well below those observed in 2022.

Growth, Inflation, and Central Banks: Differing Impacts

Oil shocks invariably place central banks in a difficult position, as they simultaneously weigh on growth and fuel inflationary pressures. The appropriate monetary policy response is not mechanical. A widely accepted principle is to avoid reacting to the direct price effects of such shocks, as interest rates do not influence the physical supply of oil. Instead, central banks must ensure that inflation expectations remain firmly anchored over the medium term.

Given the stronger growth and inflation backdrop in the United States relative to Europe, one might have expected a more proactive stance from the Federal Reserve than from the European Central Bank. In practice, the opposite has occurred. The Fed has adopted a more assertive communication stance but has left policy unchanged, while the ECB has raised its key rates in June and appears inclined to continue. In doing so, the ECB risks responding as though it were addressing the inflationary dynamics of 2021, rather than the distinct and more complex shock of 2026, while underestimating downside risks to European growth.

Past performance is not a reliable indicator of future returns and is subject to fluctuation over time. Performance may rise or fall for investments with foreign currency exposure due to exchange rate fluctuations. Emerging markets may be subject to more political, economic or structural challenges than developed markets, which may result in a higher risk

Disclaimer

This document has been prepared by ODDO BHF for information purposes only. It does not create any obligations on the part of ODDO BHF. The opinions expressed in this document correspond to the market expectations of ODDO BHF at the time of publication. They may change according to market conditions and ODDO BHF cannot be held contractually responsible for them. Any references to single stocks have been included for illustrative purposes only. Before investing in any asset class, it is strongly recommended that potential investors make detailed enquiries about the risks to which these asset classes are exposed, in particular the risk of capital loss.

ODDO BHF

12, boulevard de la Madeleine – 75440 Paris Cedex 09 France – Phone: 33(0)1 44 51 85 00 – Fax: 33(0)1 44 51 85 10 –

www.oddo-bhf.com ODDO BHF SCA, a limited partnership limited by shares with a capital of €73,193,472 – RCS 652 027 384 Paris – approved as a credit institution by the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and registered with ORIAS as an insurance broker under number 08046444. – www.oddo-bhf.com

Author